The Bank for International Settlements (BIS) said that pension funds and other “non-bank” financial firms have more than $80 trillion in hidden off-balance sheet debt in forex swaps.

The Bank for International Settlements, which has been called the central bank for the world’s central banks, said in its latest quarterly report that the market turmoil in 2022 has been largely bypassed without major problems.

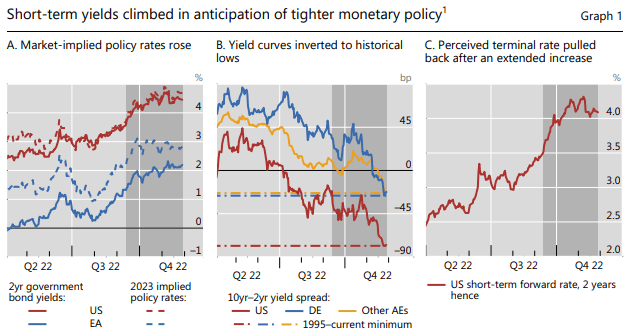

After repeatedly urging central banks to act aggressively to curb inflation, they struck a measured tone and weathered cryptocurrency market woes and UK bond market turmoil in September.

Its main warning was about what it described as a “blind spot” for foreign exchange debt that risked leaving policymakers in “the fog”.

The foreign exchange swap markets, where for example a Dutch pension fund or a Japanese insurance company borrows dollars and lends euros or yen before paying it back at a later date, has a history of problems.

They saw funding strains during the global financial crisis and again in March 2020 when the COVID-19 pandemic wreaked havoc that required central banks like the US Federal Reserve to step in on dollar swap lines.

The Bank for International Settlements said estimates of “hidden” debt of more than $80 trillion exceed dollar inventories of Treasury bonds, repurchases, and commercial paper combined. It has grown from just over $55 trillion a decade ago, while forex swap deals were nearly $5 trillion a day in April, two-thirds of daily forex trading volume.

For non-U.S. and non-U.S. banks such as pension funds, the dollar liabilities from forex swaps are now twice their dollar liabilities on the balance sheet.

“Lost dollar debt from forex/forward and currency swaps is huge,” the Swiss-based firm said, adding that the lack of first-hand information about the size and location of problems was the main issue.

closer

The report also evaluated recent developments in the broader market.

BIS officials have been vocally calling for aggressive rate hikes from central banks as inflation consolidates, but this time it took a measured tone.

Asked if the end of the tightening cycle is in sight next year, BIS Head of Monetary and Economics Claudio Borio said it will depend on how conditions evolve, also pointing to the complexities of high debt levels and uncertainty about how sensitive borrowers are now. . rates are higher.

The crisis that erupted in the UK gold markets in September also confirmed that central banks may have to step in and get involved – in the UK’s case by buying bonds even as they were raising interest rates to curb inflation.

“The simple answer is that the answer is closer than it initially was, but we don’t know how far central banks have to go,” Borio said of interest rates.

“The enemy is an old and well-known enemy,” he added, referring to inflation. “But it’s been a long time since we’ve had this fight.”

Dino mite

The report also focused on the findings of the Bank for International Settlements’ recent global foreign exchange market survey, which estimated that $2.2 trillion worth of currency deals are at risk of failing to settle on any given day due to problems between counterparties, which could undermine financial stability.

The amount at risk represents about a third of the total available forex trading volume and is more than $1.9 trillion higher than in three years prior when the last forex survey was conducted.

Foreign exchange trading also continues to shift away from multilateral trading platforms toward “less obvious” places that hinder policymakers from “appropriately monitoring currency markets,” she said.

Meanwhile, the bank’s Head of Research and Economic Adviser, Hyun Sung Shin, described recent crypto market problems such as the collapse of the FTX exchange and stablecoins, TerraUSD and Luna, as having similar characteristics to bank mishaps.

He described many of the cryptocurrencies being sold as “DINO – decentralized in name only” and that most of their related activities were done through traditional intermediaries.

“These are people who mainly take deposits in unregulated banks,” Shen said, adding that it is largely a matter of unbundling the high leverage and maturity mismatch, just as it did during the financial crash more than a decade ago.

Reporting by Mark Jones. Editing by Toby Chopra and Alexander Smith

Our standards: Thomson Reuters Trust Principles.

“Beer fan. Travel specialist. Amateur alcohol scholar. Bacon trailblazer. Music fanatic.”